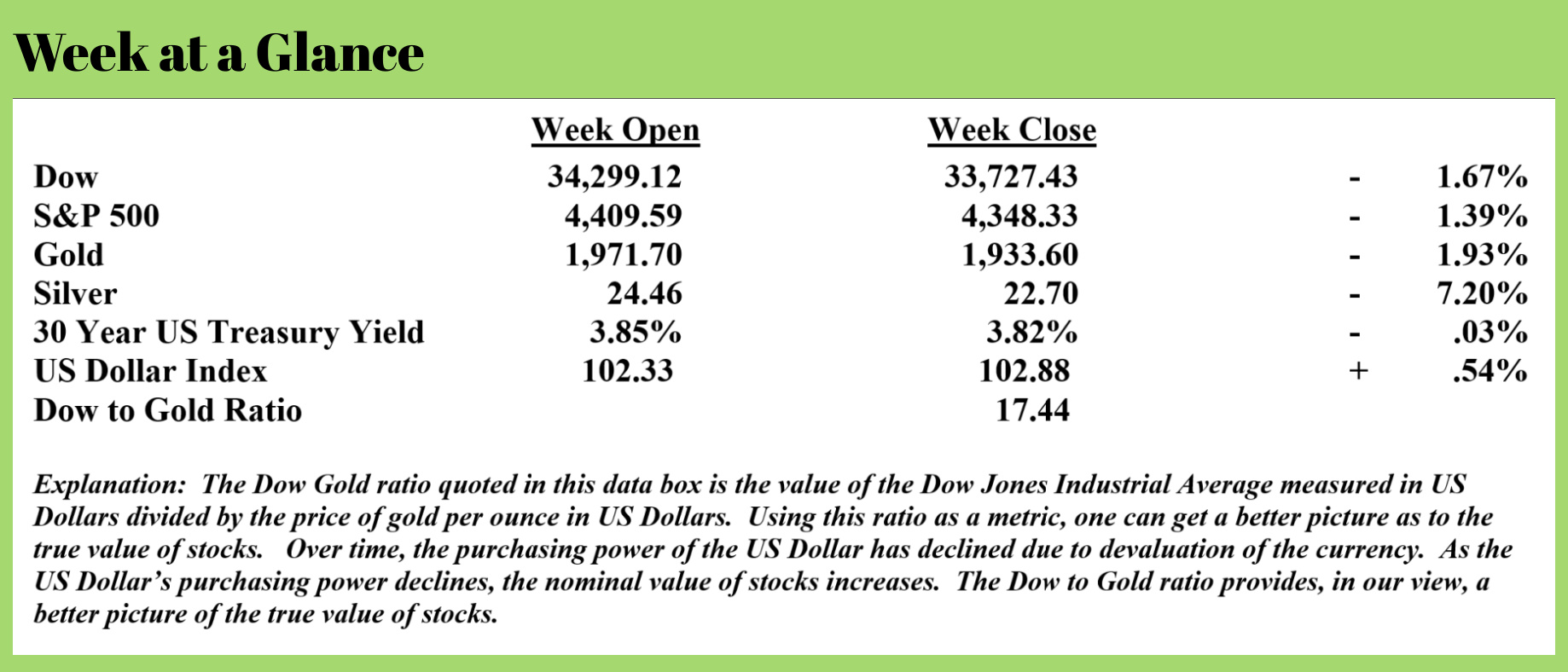

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

This week, as I was preparing my radio show and podcast, I was doing some research which led to me doing some debt math, and the result was sobering.

By way of background, I headed down this research path after discussing the current level of debt that exists in the United States, both at the national and the individual level. While I had gone through this exercise before, I wanted to do it again and in greater detail.

I’m sharing part of the research with you in this week’s “Portfolio Watch” newsletter.

The recent deal made between Biden and McCarthy was, in my view, a joke; totally form over substance. It does nothing to address the fundamental issues that, left meaningfully unaddressed, will ultimately totally undermine the US economy and the dreams of a comfortable, stress-free retirement of many Americans.

This excerpt from an article published by “MSN” explains that rather than put a new debt ceiling in place, the politicians just suspended the ceiling, allowing unlimited federal borrowing until the end of 2024 (emphasis added). (Source: https://www.msn.com/en-us/money/markets/national-debt-hits-32-trillion-two-weeks-after-debt-ceiling-deal/ar-AA1cEyZh)

Treasury Department data released Friday said federal borrowing crossed the $32 trillion mark on Thursday, less than two weeks after President Biden signed legislation into law that suspended the debt ceiling. That bill, which also included tens of billions in spending cuts demanded by House Republicans, will allow the government to borrow whatever it wants until the end of 2024, when the debt ceiling suspension ends.

When Biden signed the bill into law on June 3, the total national debt stood at $31.47 trillion. On the first business day after the debt ceiling was suspended, federal borrowing jumped nearly $400 billion, reflecting pent-up borrowing needs such as payments to federal worker retirement plans that the Treasury Department delayed in order to avoid breaching the ceiling.

As of Thursday, the national debt stood at $32.04 trillion.

Until the end of 2024, the government, unencumbered by any limit on expenditures, can spend whatever it wants.

While that’s a problem, in my view, it is far from the largest problem. It’s just exacerbating an existing, unsolvable problem – the level of debt and unfunded liabilities at the federal level.

As I’m writing this, according to debtclock.org (Source: https://www.usdebtclock.org/), the official US Government debt is just over $32 trillion. Total US debt, including federal government debt, combined state government debt, and business and household debt, stands at more than $100 trillion.

Also, according to the debt clock, the total unfunded liabilities that exist in the United States (including the massive unfunded liabilities of Social Security and Medicare) stand at more than $191 trillion.

Yes, you read that correctly. That means total debt and total unfunded liabilities stand at more than $291 trillion. Written out, that’s 291 followed by twelve, count ‘em, twelve zeros.

Census.gov tells us that the current US population is about 335 million people. Simple math tells us that equates to total debt and unfunded liabilities of more than $868,000 per person that lives in the United States.

That statistic alone is enough to clearly demonstrate that there is too much debt and there are too many unfunded liabilities to ever be paid with honest currency.

That statistic alone is enough to convince me that there will be more currency creation in the future. As I have written in many of my books, stated on my radio show and podcast, and as I teach in the “New Retirement Rules” class that I do, politicians have three choices to deal with budget shortfalls: they can increase taxes, cut spending or create currency (with help from the central bank in today’s world).

The harsh and stark reality is that this debt and unfunded liability problem is too large to be covered by taxpayers, no matter how the current or some future crop of politicians might elect to try it.

According to the Tax Foundation (Source: https://taxfoundation.org/publications/latest-federal-income-tax-data/), there were 157.5 million tax returns filed in the last year, for which we have current data. For ease in doing math, let’s call it 158 million tax returns.

If we take the $291 trillion in debt and unfunded liabilities (admittedly, some of the debt is private sector debt) and divide it by 158 million, we get nearly $1.4 million per tax return. Phrased differently, if you file a tax return, to solve this problem, you and every other person filing a US tax return would need to cough up about $1.4 million. And, even after writing that check (assuming you are financially capable of doing so), there is still a federal deficit that needs to be dealt with.

Let’s analyze this predicament another way.

If we take the $291 trillion and make the assumption that the debt and the unfunded liabilities are paid over time, and the interest rate on the unpaid balance is 5%, the collective monthly payment required of US taxpayers is $1.92 trillion, or $1,920,000,000,000!

According to the Tax Foundation (link above), the total adjusted gross income reported on all 157.5 million tax returns filed in 2020 was $12.5 trillion!

Broken down to a monthly mode, that’s a total household income of $1.042 trillion and a total monthly liability of $1.92 trillion. 100% of the income of Americans could be confiscated, and the problem is 54% solved.

This means the rhetoric-spewing politicians who want to tax billionaires are just that – revenue-spewing snake oil salespeople.

The total net worth of billionaires is about $4.5 billion, according to Statista (Source: https://www.statista.com/statistics/1291685/us-combined-value-billionaire-wealth/). That’s enough to make between 2 and 3 hypothetical payments on the debt and unfunded liability problem, as we just calculated.

While I am not going to bat for billionaires, I do possess a modicum of common sense, and since I was raised in the era of flashcards, I also have the ability to do math (even without a calculator). So, I’m not buying into the divisive, illogical, and toxic speech.

What if the politicians decide to do the responsible thing and cut spending to balance the budget?

While I think winning the lottery is way more likely than a balanced budget, let’s look at the reality of budget cuts.

The current deficit for the current fiscal year is $1.16 trillion (through the end of May with the fiscal year beginning October 1) (Source: https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/). That’s what the federal government has spent in excess of the income tax revenues collected over an 8-month time frame.

That projects a deficit of about $1.75 trillion for the year if the same deficit spending ratio holds for the last four months of the fiscal year.

According to The Peter G. Peterson Foundation (Source: https://www.pgpf.org/blog/2023/06/cbo-estimates-the-2023-deficit-will-be-15-trillion-heres-why-it-could-be-even-higher), it will cost about $700 billion for interest on the debt this year, Social Security spending will be about $1.3 trillion, and Medicare spending will be about $826 billion. Total income tax revenues are projected to be $2.5 trillion.

To balance the Federal budget, spending cuts to all programs would need to be 41% if one excludes Social Security (Source: https://thehill.com/business/budget/3900573-balancing-federal-budget-in-10-years-could-require-41-percent-cut-to-programs-when-excluding-social-security-cbo/). That number rises to cuts of 57% if Medicare is also taken off the table.

Think any of that is likely?

Not on a proactive basis, in my opinion.

But there will be a reactive reset at some point.

The eternal truth is that you can’t borrow or print your way to prosperity.

The recent prosperity we’ve seen in the economy is the result of deficit spending, which means it hasn’t been prosperity at all – it’s been a prosperity illusion.

I use the word illusion intentionally.

Webster defines illusion as something that deceives by producing a false or misleading impression of reality.

That perfectly describes the current economic environment and investing climate.

The radio program this week features an interview with Mr. Karl Denninger.

I chat with Karl about current Fed policy and why he thinks a Fed pivot or reversal is unlikely. We also talk about the inevitability of the reset and what it might look like.

You can listen to the program now by clicking on the "Podcast" tab at the top of this page.

“If I were two-faced, would I be wearing this one?”

-Abraham Lincoln

Comments